European public goods

Una unión económica que funcione bien necesita una capacidad fiscal central permanente. Esta columna sostiene que los bienes públicos europeos son una vía prometedora para que la UE lleve a cabo proyectos ejecutados a nivel centralizado mediante financiación común. Los autores elaboran una definición operativa de bienes públicos europeos y exponen formas de financiarlos y suministrarlos. Los autores reconocen que aún quedan problemas por resolver antes de que esos bienes públicos puedan ponerse en marcha a gran escala, pero proponen la próxima revisión del Marco Financiero Plurianual de la UE como una oportunidad para situarlos en el centro del debate político.

Los bienes públicos europeos (GPE) permiten a la UE llevar a cabo proyectos ejecutados a nivel centralizado mediante financiación común. Los GPE se han reactivado recientemente en el contexto de la transición ecológica y digital (Fuest y Pisani-Ferry 2019). Esta renovada atención fue impulsada por el choque pandémico, que convenció a los Estados miembros de la UE de la necesidad de crear una herramienta fiscal central, aunque de carácter temporal, en forma de NextGenerationEU (NGEU) y su componente principal, el Mecanismo de Recuperación y Resiliencia (RRF). Muchos observadores creen que el FRR debería transformarse en un instrumento permanente, creando así una capacidad fiscal central europea. Sin embargo, a pesar de su alcance innovador, el FRR se caracteriza principalmente por el uso nacional de los recursos financieros de la UE (transferencias y préstamos), ya que las negociaciones del Consejo Europeo condujeron a una reducción de la parte de los GPE (Papaconstantinou 2020). Por lo tanto, hacerlo permanente sería políticamente controvertido, ya que podría suscitar la preocupación de que la UE se esté convirtiendo en una "unión de transferencias". Este riesgo se mitigaría centrándose en la producción de GPE (Buti y Papacostantinou 2022, D'Apice y Pasimeni 2020).

https://cepr.org/voxeu/columns/european-public-goods

EPGs are less politically contentious compared to other forms of central fiscal capacity for at least two reasons. First, EPGs weaken the juste retour (or net balance) narrative, according to which each EU country tends to subtract how much it contributed to the EU budget from how much it received back directly. Second, the production of EPGs would lessen the tensions between alleged ‘creditors’ and ‘debtors’ and the consequent risks of opportunistic behaviours linked to transfers to national budgets. From a policy perspective, EPGs could help deliver the ‘triple transition’ (green, digital, social) and promote the role of the EU in international markets, thus helping to reconcile European domestic and global agendas. Furthermore, EPGs can play an important role in tackling the economic and political fallout from the Russian invasion of Ukraine.

This column is part of a long-standing research stream on EPGs that has addressed their implications for the euro area policy mix (Buti and Messori 2021a, 2022a), the role of the EU in global governance (Buti and Messori 2021b, 2022b), and the future of NGEU (Buti and Messori 2023). Against this background, in the next two sections, we put forward an operational definition of EPGs and outline a preliminary classification of these goods. We then explain how EPGs could be delivered and financed. The final section concludes.

Key features of EPGs

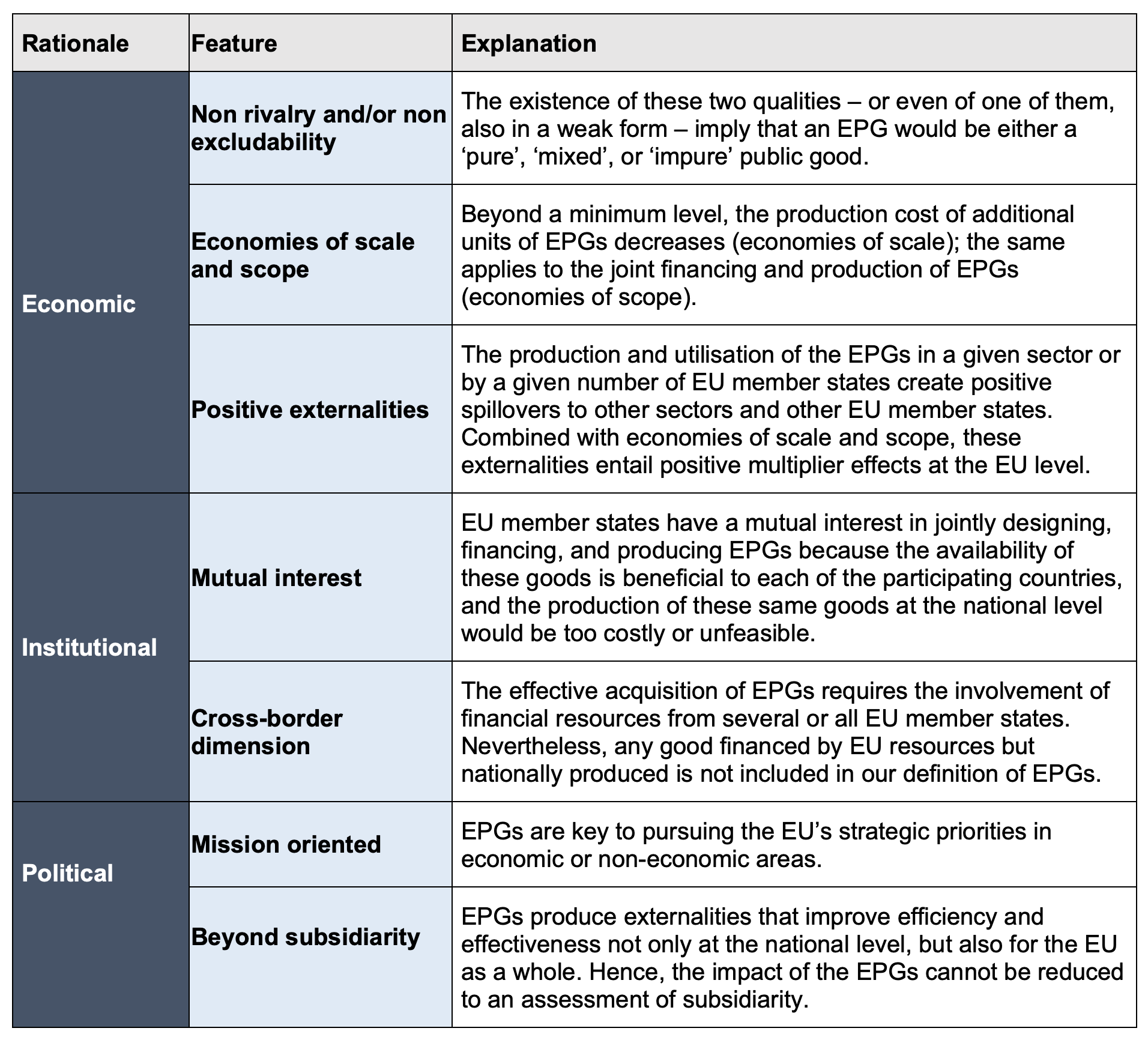

The EPGs can be interpreted as a specific application of the concept of global public goods utilised by Kindleberger (1973) and many others (Buchholz and Sandler 2021) to extend the theoretical concept of pure public goods (Samuelson 1954 and 1955, Buchanan 1968) to the activities involved in the integration of international markets. This extension implies that the classical analysis of public goods has been grafted onto other strands of economic literature, namely, the theory of fiscal federalism. It has also weakened some of the original features of the public goods concept. Being a specific version of global public goods, EPGs require a further operational definition. We thus define three broad rationales for that definition: economic, institutional, and political. 1

According to the economic rationale, a ‘pure’ public good is characterised by two main features: first, its utilisation by an additional beneficiary has a marginal cost approaching zero (non-rivalrous); and second, the exclusion of a potential beneficiary is either impossible or very inefficient (non-excludable). These two features have an important implication: market mechanisms tend to supply an insufficient amount of ‘pure’ public goods because a profit-maximising producer of this type of goods would bear the full costs but could internalise only a portion of the benefits (e.g. Stiglitz 1986). Hence, the creation of an efficient amount of public goods requires a direct or indirect public intervention.

At the global level, an undersupply applies not only to ‘pure’ public goods, but also to goods that satisfy only one of the two criteria above or even just a weak formulation of (one of) these same criteria. In the former case, the economic literature refers to ‘mixed’ public goods; in the latter, to ‘impure’ public goods. Hence, the three types of public goods share the crucial feature mentioned above: that of giving rise to market failures. This feature is strengthened by two related and key characteristics of public goods: their ability to generate economies of scale and spillovers (positive externalities). Being a specific version of global public goods, EPGs incorporate all these features. Hence, for the purposes of this column, we define EPGs as ‘pure’, ‘mixed’, and ‘impure’ public goods producing positive externalities thanks mainly to centralised public interventions.

As to the institutional rationale for identifying EPGs, two additional specificities emerge. First, the production and financing of a given good or service take place optimally at the EU level, as the added value of this same good or service increases when it is the outcome of a joint design and a common effort of the EU members. This feature leads to the second institutional aspect of the EPGs: it is in the mutual interest of the member states to exploit the cross-border dimension to prepare, support, and implement the production of these goods and services.

Finally, according to the political rationale, EPGs should benefit the EU as a political entity and not only as the sum of its individual member states. EPGs should strengthen the cohesion across countries and buttress citizens’ support of European cooperation. We label these features as ‘beyond subsidiarity’ to emphasise their multiplicative effects. Finally, EPGs should be ‘mission oriented’ by supporting the EU’s strategic domestic and international political priorities.

The economic, institutional, and political rationales for EPGs analysed above are ‘translated’ in the seven features illustrated in Table 1. 2

Table 1 Main features of EPGs

Source: Authors’ elaboration.

Identifying EPGs

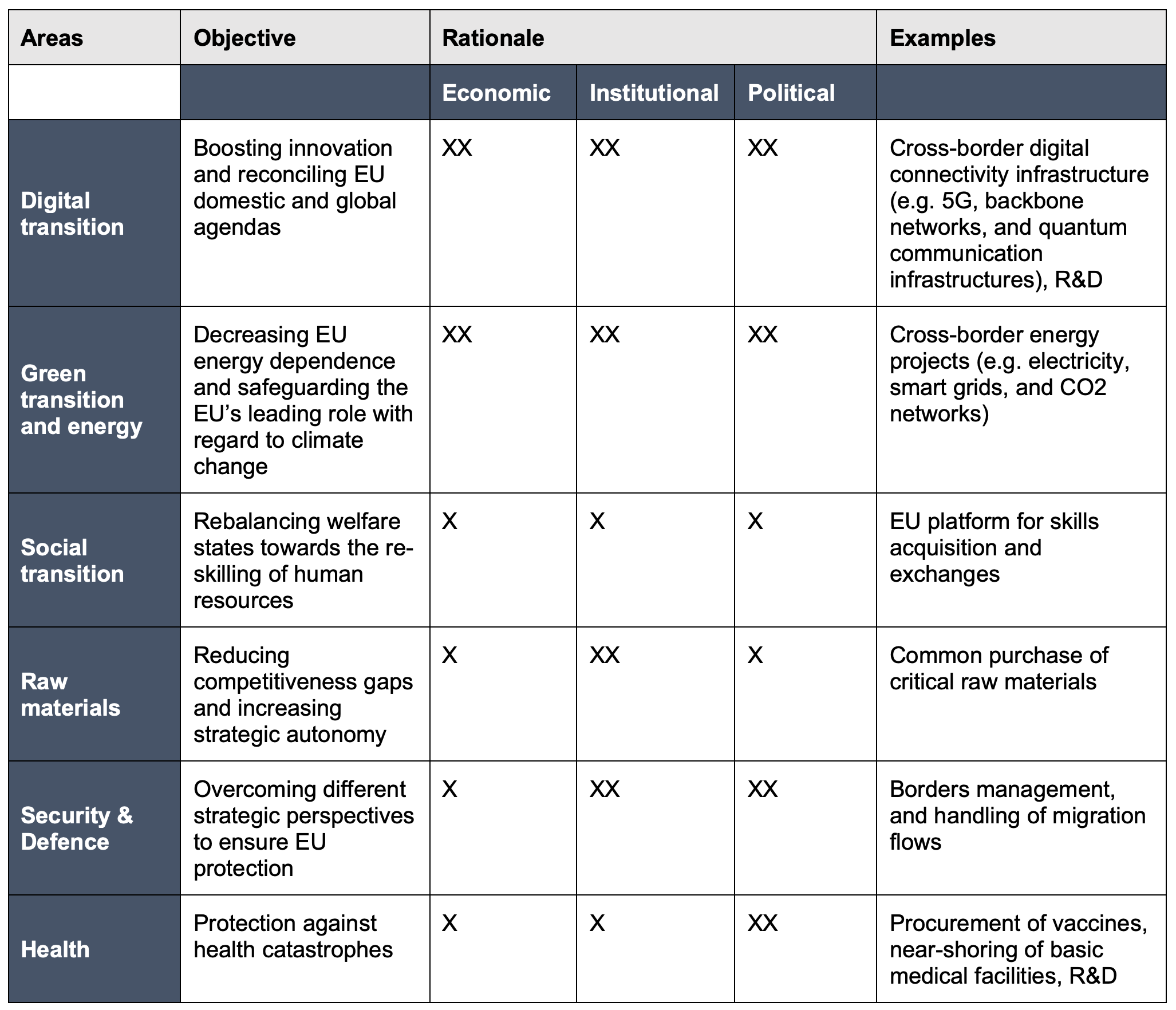

Based on the analysis in the previous section, in Table 2 we identify six priority areas: the digital transition, the ‘green’ transition and energy, the social transition, raw materials, security and defence, and health. 3 For each area, we provide a subjective assessment of compliance with the three rationales mentioned above, and we indicate some non-exhaustive examples of specific EPGs that meet their corresponding objectives.

Table 2 A classification of EPGs

Source: Authors’ elaboration.

The first four challenges pertain to the economic field: (1) reaching climate neutrality to preserve the EU’s international leadership in terms of low environmental impact and ‘circular economy’; (2) reducing the EU’s technological gaps towards the US and China and innovating the EU production model by means of a centralised industrial policy (Buti and Messori 2023); (3) improving education and re-skilling as necessary conditions to successfully pursue the double transition without weakening European social protection; and (4) buttressing the EU’s open strategic autonomy as part of a renewed system of multilateral governance. These four challenges call for the supply of EPGs in areas such as digital transition (cross-border digital connectivity infrastructure), ‘green’ transition and renewable energy (cross-border energy projects), labour market and social transition (platforms for skills acquisitions), and the strategic raw materials required for innovative productions.

Additionally, the experience with Covid-19 calls for EU interventions in health, from the centralisation in the purchase of vaccines to the near-shoring of basic medical facilities and the centralisation of innovative medical research. Finally, the war at the EU’s eastern borders and the human drama affecting large parts of Africa and the Middle East point to the need for EPGs in the areas of defence and security. Examples are the inclusive management of migration flows and the protection of the EU’s external borders.

In Table 2, we provide a subjective assessment of the compliance of the six areas with the economic, institutional, and political criteria identified in Table 1. A double cross (XX) denotes high potential; a single cross (X) denotes satisfactory potential. Whilst most projects listed in this Table would qualify as EPGs according to our definition based on the number of crosses, the three areas which emerge as critical for the supply of EPGs are the digital transition, ‘green’ transition and energy, and security and defence.

Financing and delivering EPGs

To finance and deliver EPGs, it is necessary to put in place a permanent central fiscal capacity because the common EU projects discussed above have a medium to long-term dimension. The creation of a permanent central fiscal capacity raises difficult legal and institutional questions that go beyond the scope of this paper. According to Tosato (2021), the EU treaties are sufficiently flexible to include a ‘recurrent’ central fiscal capacity as a tool of managing repeated external shocks. We therefore focus on questions of how to finance and deliver these goods.

NGEU and the SURE programmes offer two different options for the financing of a temporary central fiscal capacity. The former allows the European Commission to issue European bonds in the financial markets on behalf of the EU thanks to the guarantees offered by the headroom of the ‘own resources’ ceiling. The latter entitles the European Commission to issue bonds backed by national guarantees that are offered by the euro area member states. However, these direct or indirect guarantees cannot work in the case of a permanent or recurrent central fiscal capacity, as required by the production of EPGs. The extension of these guarantees to a very long (or even infinite) horizon would imply implicit and growing liabilities for national budgets that would impose binding constraints on national fiscal policies. Hence, the financing of EPGs requires that the central level be endowed with specific tax bases or, in the EU’s terminology, new ‘own resources’. This task is fraught with difficulties, as the modest progress in the enlargement of European taxation since the publication of the Monti report shows (Monti et al. 2016). The forthcoming proposals by the European Commission on a new corporate taxation basis (BEFIT) offers an opportunity to define more robust new ‘own resources’. 4

Even if it were possible to solve the problem of centralised financing for the EPGs, there would remain the issue of their effective delivery. A pragmatic idea would be to rely on the vehicles offered by EU programmes – either new versions or those already in place. In this respect, while the RRF and SURE cannot play a role as EPG vehicles – because their projects are implemented at the national level even when centrally financed – there are other EU programmes that can serve the purpose of delivering EPGs. Some parts of the RePower-EU support common initiatives at the EU level; the same applies to a few programmes of NGEU such as Connecting Europe Facility, InvestEU, and Horizon. European initiatives are also the core of the Innovation Fund and the Hydrogen Bank. Moreover, if reformed to allow financing via EU resources and devoted to genuinely EU-wide projects, the Important Projects of Common European Interest (IPCEI) would offer a very useful tool. Finally, it may be necessary to create other EU vehicles, such as the EU Sovereignty Fund put forward by the President of the European Commission in the State of the Union speech in September 2022. This would also serve as a way to bring together the various separate vehicles mentioned above under a unified and visible policy instrument.

Conclusion

A well-functioning economic union needs a permanent central fiscal capacity. Amongst the various options, stepping up the supply of EPGs delivered and financed at the EU level appears the most promising avenue to create a central fiscal capacity in the EU. We have argued that EPGs should meet a number of criteria at the intersection of the economic theory of public goods, the theory of fiscal federalism, and the specific institutional and political features of the EU.

We have provided a preliminary conceptual framework that helps define and select EPGs. In particular, we have listed a number of characteristics under three main rationales: economic, institutional, and political. Against this background, we have identified six policy areas (digital transition, green transition and energy, social transition, raw materials, security and defence, and health) that respond to the main challenges the EU is facing. We have listed a number of specific projects and suggested how they could be financed and delivered at the EU level. Creating EPGs in these areas would help the EU economy tackle the growing innovation gap vis-à-vis the US and China in digital activities and artificial intelligence, buttress its energy autonomy, and hence shift the EU economy onto a more sustainable ‘business model’.

In our view, the case for increasing the supply of EPGs is strong. However, the debate on EPGs so far –and, more generally, on a central fiscal capacity – has not taken centre stage for at least two reasons. First, a large amount of resources remains to be spent following the successful implementation of the national recovery and resilience plans. It is hard to conceive of creating a permanent or recurrent central fiscal capacity without the clear success of the RRF. Second, the European Commission has decided to strategically decouple the discussion on the reforms of the fiscal rules from the discussion of a central fiscal capacity because it might be easier to agree on new fiscal rules without overburdening an already difficult conversation with further controversial elements. In the short term, this decoupling is understandable, but in the longer run the credibility and success of a rules-based fiscal framework depends on nesting a central fiscal capacity into the new economic governance model.

The conditions for supplying an adequate amount of EPGs are not yet fulfilled. However, this does not mean that the debate on EPGs should be postponed to an indefinite future. The upcoming review of the Multiannual Financial Framework provides an opportunity for bringing the EPGs to the centre of the policy debate. The adaptation of a number of EU ‘vehicles’ and the proposal to create an EU Sovereignty Fund should be framed as the initial steps in rebalancing the EU budget from transfers to the supply of EPGs.

Authors’ note: The authors write in their personal capacity.

References

Buchholz, W and T Sandler (2021), “Global public goods: A survey”, Journal of Economic Literature 59(2): 488–545.

Buchanan, J (1968), The demand and supply of public goods, Chicago: Rand McNally.

Buti, M and M Messori (2021a), “The search for a congruent euro area policy mix: Vertical coordination matters”, CEPR Policy Insight No. 113.

Buti, M and M Messori (2021b), “Towards a new international economic governance: The possible role of Europe”, STG Policy Papers, School of Transnational Governance, November.

Buti, M and M Messori (2022a), “A central fiscal capacity in the EU policy mix”, CEPR Discussion Paper 17577.

Buti, M and M Messori (2022b), “The role of central fiscal capacity in connecting the EU’s domestic and global agendas”, STG Policy Papers, EUI School of Transnational Governance, June.

Buti, M and M Messori (2023), “Resetting the EU’s business model after the watershed”, EPC Discussion Paper, 13 February.

Buti, M and G Papaconstantinou (2022), “European public goods: How can we supply more”, VoxEU.org, 31 January.

D’Apice, P and P Pasimeni (2023), “Financing EU public goods: Vertical coherence between EU and national budgets”, EUI RSCAS, 2020/47.

Fuest, C and J Pisani-Ferry (2019), A primer on developing European public goods, EconPol Policy Report, Vol. 3, 16 November.

Kindleberger, C P (1973), The World in Depression: 1929–1939, University of California Press.

Monti, M et al. (2016), “Future financing of the EU. Final report and recommendations of the High-Level Group on own resources”, Brussels, December.

Papaconstantinou, G (2020), “European public goods: just a buzzword or a new departure?”, in Realising European Added Value, ECA Journal, 2020/3.

Samuelson, P A (1954), “The pure theory of public expenditure”, Review of Economics and Statistics 36(4): 387–89.

Samuelson, P A (1955), “Diagrammatic exposition of a theory of public expenditure”, Review of Economics and Statistics 37(4): 350–56.

Stiglitz, J E (1986), Economics of the Public Sector, New York: W. W. Norton.

Stiglitz, J E (1999), “Knowledge as a Global Public Good”, Global Public Goods: International Cooperation in the 21st Century, Oxford University Press, 308–25.

Thöne, M and H Kreuter (2020), “European public goods: Their contribution to a strong Europe”, Bertelsmann Stiftung Vision Europe Paper, 3 September.

Tosato, G L (2021), “Sulla fattibilità giuridica di una capacità fiscale della UE a Trattati costanti,” Astrid Rassegna, n. 15.

Footnotes

- For a similar attempt to specify EPGs criteria, see Thöne and Kreuter (2020).

- It should be noted that our analysis of EPGs is focused on ‘material’ public goods (and services), i.e. on those EPGs based on investment and production processes. Hence, we leave the crucial issue of the allocation of knowledge as a global public good (Stiglitz 1999) in the background, and we neglect the EPGs mainly due to reforms and ‘immaterial’ outcomes (e.g. a positive externality such as financial stability).

- A partly similar classification was elaborated, before the pandemic, by Fuest and Pisani-Ferry (2019).

- The lack of an independent source of EU revenue to back the issuance of European bonds to finance NGEU may partly explain the recent underperformance of such bonds in financial markets.

No hay comentarios:

Publicar un comentario