31 Premios Fronteras han ganado posteriormente el Nobel

Nobel de Economía para Daron Acemoglu, ganador del Premio Fronteras del Conocimiento en 2016

Daron Acemoglu, galardonado con el Premio Fundación BBVA

Fronteras del Conocimiento en Economía, Finanzas y Gestión de Empresas

en su IX edición, ha ganado hoy el Premio del Banco de Suecia en

Ciencias Económicas en memoria de Alfred Nobel 2024 junto a Simon

Johnson y James Robinson. El jurado les ha concedido este reconocimiento

por demostrar la importancia de las instituciones sociales para la

prosperidad de un país.

14 octubre, 2024

El acta del premio ha destacado que las investigaciones de los

galardonados ayudan a comprender por qué “las sociedades con un Estado

de Derecho deficiente e instituciones que explotan a la población no

generan crecimiento ni cambios a mejor”. Además, ha remarcado que su

trabajo ha demostrado que “una de las explicaciones de las diferencias

en la prosperidad de los países son las instituciones sociales que se

introdujeron durante la colonización”, subrayando la relevancia de las

instituciones inclusivas para el desarrollo de poblaciones prósperas y

la consolidación de las instituciones democráticas.

“Reducir las enormes diferencias de renta entre países es uno de los

mayores retos de nuestro tiempo. Los galardonados han demostrado la

importancia de las instituciones sociales para lograrlo”, ha afirmado

Jakob Svensson, Presidente del Comité del Premio de Ciencias Económicas.

En 2016, Acemoglu (Estambul, 1967) recibió el Premio Fundación BBVA Fronteras del Conocimiento en Economía, Finanzas y Gestión de Empresas.

El jurado destacó en aquella ocasión su contribución “por ayudar a

comprender los determinantes del desarrollo económico a largo plazo, con

especial énfasis en la importancia que tienen sobre éste las

instituciones y la organización de la sociedad. Lo novedoso de la

aportación de Acemoglu fue desarrollar una estrategia para encontrar

evidencia empírica, lo que le permitió establecer el efecto causal de

las instituciones sobre el desarrollo”.

“Para lograr un crecimiento económico sostenido se necesita

innovación y creatividad”, defendió Acemoglu en una entrevista concedida

tras el anuncio de su Premio Fronteras del Conocimiento. “La

importancia del papel que juega la tecnología, por ejemplo, o el de la

educación se comprenden bien”, aseveró el premiado, “pero lo que faltaba

era preguntarse por qué las naciones no invierten más en educación o

por qué no fomentan la adopción de las mejores tecnologías existentes”.

Estas decisiones, que conforman las instituciones propias de cada

sociedad, son determinantes para el grado de desarrollo económico de un

país. El desarrollo de este concepto de instituciones y el

establecimiento de su relación causal sobre el desarrollo económico es

lo que le valió a Acemoglu el Premio Fronteras del Conocimiento en 2016 y

que ha sido reconocido ahora por la institución sueca.

En 2012, Acemoglu publicó ¿Por qué fracasan las naciones? Orígenes del poder, la prosperidad y la pobreza

junto a James Robinson, también reconocido por los Premios Nobel en

esta edición. En él, profundizan en el concepto de instituciones

inclusivas, aquellas que incentivan la inversión y la innovación y

proporcionan igualdad de condiciones. En contraposición, definen las

instituciones extractivas como aquellas que “crean derechos de propiedad

volátiles, dificultan los contratos, desaniman la innovación y la

incorporación de tecnología y, lo que es más importante, generan normas

que benefician a un pequeño segmento de la sociedad, llegando incluso a

trabajar por sueldos muy bajos o a impedir el acceso a determinadas

ocupaciones”.

Los autores concluyeron que “no hay una manera fácil” de realizar la

transición de una sociedad basada en instituciones extractivas a

inclusivas, aunque reconocieron “que tampoco hemos encontrado otro modo

de asegurar la prosperidad a largo plazo”.

Una trayectoria pionera

Daron Acemoglu se graduó en la Universidad de York (Reino Unido) en

1989 y se doctoró en 1992 en la London School of Economics, donde

ejerció como profesor durante un año. En 1993, se convirtió en miembro

del Instituto Tecnológico de Massachusetts (MIT) donde actualmente ocupa la Cátedra Elizabeth and James Killian de Economía.

Ha publicado más de un centenar de artículos en revistas

internacionales como ‘American Economic Review’, el ‘Quarterly Journal

of Economics’ o ‘Review of Economic Studies’, además de cuatro libros.

Es miembro de la Academia Americana de las Artes y las Ciencias, de la

Asociación Económica Europea y de la Econometric Society. Además, con

solo 44 años fue director de la revista ‘Econometrica’.

Durante su trayectoria profesional ha recibido numerosas

distinciones, entre las que destacan la medalla John Bates Clark, que la

Asociación Americana de Economía otorga cada dos años al economista

estadounidense más influyente menor de cuarenta años, y que Acemoglu

recibió en 2005.

31 Premios Fronteras han ganado posteriormente el Nobel

Tras la concesión del Premio Nobel de Economía a Daron Acemoglu, son

ya 31 los galardonados con Premios Fronteras del Conocimiento que

posteriormente han ganado un Nobel.

Daron Acemoglu, Simon Johnson y James A. Robinson ganan el Nobel de Economía

La Academia destaca que los galardonados han

demostrado la importancia de las instituciones sociales para la

prosperidad de los países

La Real Academia Sueca de

Ciencias ha decidido otorgar el Premio Sveriges Riksbank en Ciencias

Económicas en memoria de Alfred Nobel 2024 a Daron Acemoglu, Simon

Johnson y James A. Robinson «por sus estudios sobre cómo se forman las

instituciones y cómo afectan la prosperidad».

Según ha destacado la institución, avanza Europa Press,

los galardonados este año han demostrado la importancia de las

instituciones sociales para la prosperidad de un país y han ayudado a

comprender por qué las sociedades con un Estado de derecho deficiente e

instituciones que explotan a la población no generan crecimiento ni

cambios para mejor.

En este sentido, los

trabajos de los galardonados han demostrado que una de las explicaciones

de las diferencias en la prosperidad de los países «son las

instituciones sociales que se introdujeron durante la colonización», que

para la Academia es una razón importante de por qué las antiguas

colonias que una vez fueron ricas ahora son pobres, y viceversa.

«Algunos países quedan

atrapados en una situación de instituciones extractivas y bajo

crecimiento económico. La introducción de instituciones inclusivas

crearía beneficios a largo plazo para todos, pero las instituciones

extractivas proporcionan ganancias a corto plazo para las personas en el

poder», explica.

«Reducir las enormes

diferencias de ingresos entre los países es uno de los mayores desafíos

de nuestro tiempo. Los galardonados han demostrado la importancia de las

instituciones sociales para lograrlo», ha destacado Jakob Svensson,

presidente del Comité del Premio de Ciencias Económicas.

Daron Acemoglu, nacido en

1967 en Estambul (Turquía), es profesor en el Instituto Tecnológico de

Massachusetts (EE.UU.), igual que el británico Simon Johnson, nacido en

1963, mientras que James A. Robinson, nacido en 1960, es profesor en la

Universidad de Chicago y publicó junto a Acemoglu en 2012 el influyente

libro ‘Por qué fracasan los países: Los orígenes del poder, la

prosperidad y la pobreza’.

El desafío de China

En sus primeras

declaraciones posteriores al anuncio del galardón, Daron Acemoglu, ha

reconocido desde Atenas estar «encantado», conmocionado, sorprendido con

la noticia, que le ha supuesto «un verdadero shock» y un «honor»

«Uno nunca espera algo

así», ha admitido Acemoglu, cuyo nombre ha estado en los últimos años en

las quinielas para el Nobel. «Creo que fue Napoleón quien dijo que,

cuando uno entra en la escuela de cadetes, sueña con convertirse en

general, pero no en presidente o rey», ha añadido.

En cuanto a las razones

que la Academia sueca ha esgrimido para conceder el galardón de este

año, el economista ha defendido que los países que se democratizan a

partir de un régimen no democrático terminan creciendo en unos ocho o

nueve años más rápido que los regímenes no democráticos, aunque ha

advertido de que «la democracia no es una panacea».

En este sentido, ha

recordado que introducir la democracia es muy difícil y, en particular,

en sociedades ya polarizadas, las elecciones pueden conducir a

resultados de corta duración que a veces no son de naturaleza

democrática en el sentido de que un partido gana el poder e implementa

las cosas de manera autoritaria, mientras que hay vías por las que los

países no democráticos pueden realmente crecer.

«Es algo que James

Robinson y yo hemos enfatizado mucho en nuestro libro, ‘Por qué fracasan

las naciones’, lo que llamamos crecimiento extractivo», ha explicado

Acemoglu en referencia a que estos países pueden movilizar rápidamente

recursos para sus sectores y empresas existentes, lo que puede conducir a

una recuperación del crecimiento.

Sin embargo, el economista

de origen turco ha defendido que este tipo de crecimiento autoritario

es a menudo más inestable y no suele conducir a una innovación muy

rápida y original, añadiendo que, si bien «China es un desafío», bajo su

perspectiva estos regímenes autoritarios, por diversas razones, van a

tener más dificultades para lograr resultados de innovación sostenibles a

largo plazo.

This year’s laureates have provided new insights into why there are such

vast differences in prosperity between nations. One important

explanation is persistent differences in societal institutions. By

examining the various political and economic systems introduced by

European colonisers, Daron Acemoglu, Simon Johnson and James Robinson

have been able to demonstrate a relationship between institutions and

prosperity. They have also developed theoretical tools that can explain

why differences in institutions persist and how institutions can change.

14 October 2024

“for studies of how institutions are formed and affect prosperity”

They have helped us understand differences in prosperity between nations

Los galardonados de este año en ciencias económicas - Daron Acemoglu, Simon Johnson y James Robinson - han demostrado la importancia de las instituciones sociales para la prosperidad de un país. Las sociedades con un Estado de Derecho deficiente e instituciones que explotan a la población no generan crecimiento ni cambios a mejor. Las investigaciones de los galardonados nos ayudan a entender por qué.

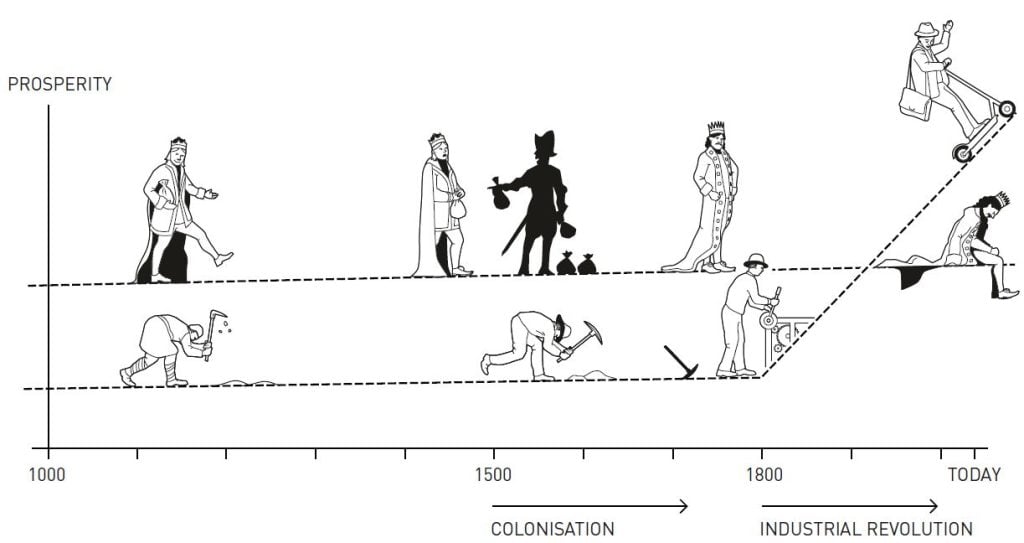

Cuando los europeos colonizaron grandes zonas del planeta, las instituciones de esas sociedades cambiaron. El cambio fue a veces drástico, pero no se produjo de la misma manera en todas partes. En algunos lugares, el objetivo era explotar a la población indígena y extraer recursos en beneficio de los colonizadores. En otros, los colonizadores crearon sistemas políticos y económicos integradores para beneficio a largo plazo de los emigrantes europeos.

Los galardonados han demostrado que una de las explicaciones de las diferencias en la prosperidad de los países son las instituciones sociales que se introdujeron durante la colonización. A menudo se introdujeron instituciones inclusivas en países que eran pobres cuando fueron colonizados, lo que con el tiempo dio lugar a una población generalmente próspera. Esta es una razón importante de por qué las antiguas colonias que antes eran ricas ahora son pobres, y viceversa.

Some countries become trapped in a situation with extractive

institutions and low economic growth. The introduction of inclusive

institutions would create long-term benefits for everyone, but

extractive institutions provide short-term gains for the people in

power. As long as the political system guarantees they will remain in

control, no one will trust their promises of future economic reforms.

According to the laureates, this is why no improvement occurs.

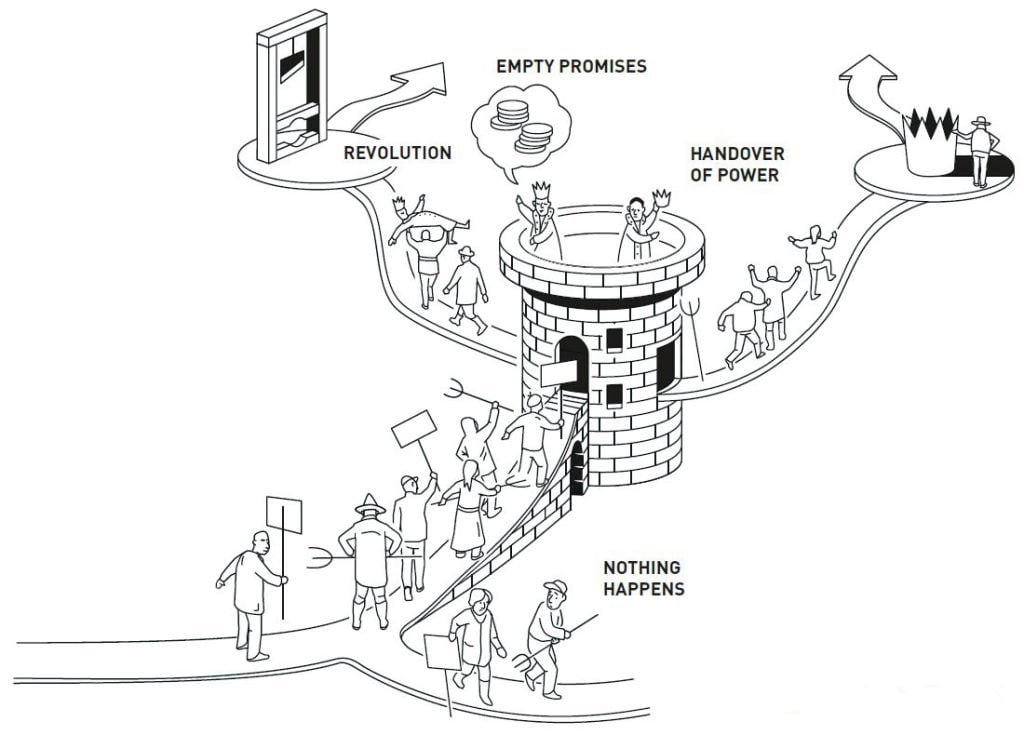

Sin embargo, esta incapacidad para hacer promesas creíbles de cambio positivo también puede explicar por qué a veces se produce la democratización. Cuando existe una amenaza de revolución, los gobernantes se enfrentan a un dilema. Preferirían permanecer en el poder e intentar aplacar a las masas prometiendo reformas económicas, pero es poco probable que la población crea que no volverán al viejo sistema en cuanto se calme la situación. Al final, la única opción puede ser transferir el poder e instaurar la democracia.

"Reducir las enormes diferencias de renta entre países es uno de los mayores retos de nuestro tiempo. Los galardonados han demostrado la importancia de las instituciones sociales para lograrlo", afirma Jakob Svensson, Presidente del Comité del Premio de Ciencias Económicas.

They provided an explanation for why some countries are rich and others poor

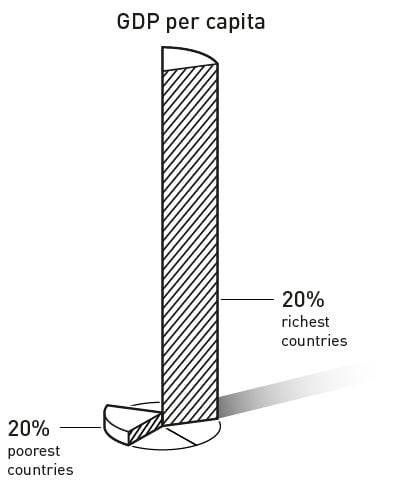

El 20% de los países más ricos del mundo son ahora unas 30 veces más ricos que el 20% más pobre. Además, la diferencia de ingresos entre los países más ricos y los más pobres es persistente; aunque los países más pobres se han enriquecido, no están alcanzando a los más prósperos. ¿Por qué? Los galardonados de este año han encontrado pruebas nuevas y convincentes de una de las explicaciones de esta brecha persistente: las diferencias en las instituciones de una sociedad.

Providing evidence for this is no easy task. A correlation between

the institutions in a society and its prosperity does not necessarily

mean that one is the cause of the other. Rich countries differ from poor

ones in many ways – not just in their institutions – so there could be

other reasons for both their prosperity and their types of institutions.

Perhaps prosperity affects a society’s institutions, rather than

vice-versa. To arrive at their answer, the laureates used an innovative

empirical approach.

Acemoglu, Johnson y Robinson examinaron la colonización europea de amplias zonas del planeta. Una explicación importante de las actuales diferencias de prosperidad son los sistemas políticos y económicos que los colonizadores introdujeron, o decidieron mantener, a partir del siglo XVI. Los galardonados demostraron que esto condujo a una inversión de la fortuna. Los lugares que eran, en términos relativos, los más ricos en el momento de su colonización se encuentran ahora entre los más pobres. Además, utilizaron cifras de mortalidad de los colonizadores, entre otras cosas, y descubrieron una relación: a mayor mortalidad entre los colonizadores, menor PIB per cápita actual. ¿A qué se debe? La respuesta es que la mortalidad de los colonos (lo "peligroso" que era colonizar una zona) afectaba a los tipos de instituciones que se creaban.

The laureates have also developed an innovative theoretical framework

that explains why some societies become stuck in a trap with what the

laureates call extractive institutions, and why escaping from this trap

is so difficult. However, they also show that change is possible and

that new institutions can be formed. In some circumstances, a country

can break free of its inherited institutions to establish democracy and

the rule of law. In the long run, these changes also lead to reduced

poverty.

How can we see the traces of these colonial institutions in the

present day? In one of their works, the laureates use the city of

Nogales, on the border between the USA and Mexico, as an example.

A tale of two cities

Nogales is cut in half by a fence. If you stand by this fence and

look north, Nogales, Arizona, USA stretches out ahead of you. Its

residents are relatively well off, have long average lifespans and most

children receive high school diplomas. Property rights are secure and

people know they will get to enjoy most of the benefits from their

investments. Free elections provide residents with the opportunity to

replace politicians with whom they are not satisfied.

If you look south instead, you see Nogales, in Sonora, Mexico. Even

though this is a relatively wealthy part of Mexico, the residents here

are in general considerably poorer than on the north side of the fence.

Organised crime makes starting and running companies risky. Corrupt

politicians are difficult to remove, even if the chances of this have

improved since Mexico democratised, just over 20 years ago.

¿Por qué estas dos mitades de la misma ciudad tienen condiciones de vida tan diferentes? Geográficamente están en el mismo lugar, por lo que factores como el clima son exactamente iguales. Las dos poblaciones también tienen orígenes similares; históricamente, la zona norte estaba en realidad en México, por lo que los residentes de larga duración de la ciudad tienen muchos antepasados comunes. También hay muchas similitudes culturales. La gente come parecido y escucha más o menos el mismo tipo de música a ambos lados de la valla.

Traducción realizada con la versión gratuita del traductor DeepL.com

La diferencia decisiva no es, pues, la geografía o la cultura, sino las instituciones. Las personas que viven al norte de la valla viven en el sistema económico de EE.UU., que les da mayores oportunidades de elegir su educación y profesión. También forman parte del sistema político estadounidense, que les otorga amplios derechos políticos. Al sur de la valla, los residentes no son tan afortunados. Viven en otras condiciones económicas, y el sistema político limita sus posibilidades de influir en la legislación. Los galardonados de este año han demostrado que la dividida ciudad de Nogales no es una excepción. Al contrario, forma parte de un claro patrón con raíces que se remontan a la época colonial.

Colonial institutions

Cuando los europeos colonizaron grandes partes del mundo, las instituciones existentes cambiaron a veces drásticamente, pero no de la misma manera en todas partes. En algunas colonias, el propósito era explotar a la población indígena y extraer recursos naturales en beneficio de los colonizadores. En otros casos, los colonizadores construyeron sistemas políticos y económicos integradores para beneficio a largo plazo de los colonos europeos.

Un factor importante que influyó en el tipo de colonia que se desarrolló fue la densidad de población de la zona que se iba a colonizar. Cuanto más densa era la población indígena, mayor era la resistencia que cabía esperar. Por otro lado, una población indígena más numerosa -una vez derrotada- ofrecía oportunidades lucrativas de mano de obra barata. El resultado fue que menos colonos europeos se trasladaron a colonias ya densamente pobladas. Los lugares más escasamente poblados ofrecían menos resistencia a los colonizadores y menos mano de obra que explotar, por lo que más colonizadores europeos se trasladaron a estos lugares escasamente poblados.

A su vez, esto influyó en los sistemas políticos y económicos que se desarrollaron. Cuando había pocos colonizadores, éstos se hacían con el poder o establecían instituciones extractivas que se centraban en beneficiar a una élite local a expensas de la población en general. No había elecciones y los derechos políticos eran muy limitados. En cambio, las colonias con muchos colonizadores -colonias de colonos- necesitaban instituciones económicas inclusivas que incentivaran a los colonos a trabajar duro e invertir en su nueva patria. A su vez, esto llevaba a exigir derechos políticos que les dieran una parte de los beneficios. Por supuesto, las primeras colonias europeas no eran lo que hoy llamaríamos democracias pero, en comparación con las colonias densamente pobladas a las que se trasladaban pocos europeos, las colonias de colonos ofrecían derechos políticos considerablemente más amplios.

Reversal of fortune

Los galardonados de este año han demostrado que estas diferencias iniciales en las instituciones coloniales son una explicación importante de las grandes diferencias de prosperidad que vemos hoy en día. Las diferencias actuales en las condiciones de vida entre Nogales (Estados Unidos) y Nogales (México) se deben en gran medida a las instituciones que se introdujeron en la colonia española que más tarde se convirtió en México y en las colonias que se convirtieron en Estados Unidos. Este patrón es similar en todo el mundo colonizado y no depende de si los colonizadores fueron británicos, franceses, portugueses o españoles.

Paradoxically, this means that the parts of the colonised world that

were relatively the most prosperous around 500 years ago are now those

that are relatively poor. If we look at urbanisation as a measure of

prosperity, this was greater in Mexico under the Aztecs than it was at

the same time in the part of North America that is now called Canada and

the USA. The reason is that in the poorest and most sparsely populated

places, European colonisers introduced or kept institutions that

promoted long-run prosperity. However, in the richest and most densely

populated colonies, institutions were more extractive and – for the

local population – less likely to lead to prosperity.

This reversal of relative prosperity is historically unique. When the

laureates studied urbanisation in the centuries prior to colonisation,

they did not find a similar pattern: the more urban and thus richer

parts of the world remained more urban and richer. In addition, if we

look at the parts of the globe that were not colonised, we do not find any reversal of fortune.

The laureates have also shown that this reversal mainly occurred in

association with the industrial revolution. As late as the

mid-eighteenth century, for example, industrial production in what is

now India was higher than in the USA. This has changed fundamentally

since the start of the nineteenth century, which speaks to the reversal

primarily being a result of differences in institutions. The technical

innovations sweeping across the world were only able take hold in places

where institutions had been established that would benefit the wider

population.

Settler mortality

The most direct explanation for the type of colonial institutions was

thus the number of European settlers. The more European settlers, the

greater the probability of establishing economic systems that promoted

long-run economic growth. The laureates have shown that another factor

that contributed to institutional differences was the severity of the

diseases that spread through the settler communities.

The prevalence of deadly disease varied greatly between the northern

and southern areas of America, just as in African regions that are

closer to the equator than the southernmost regions. Similarly, the

diseases that were found in India were considerably more numerous and

dangerous to the British colonisers than those in New Zealand or

Australia. The incidence of disease, which can be seen in historical

statistics of mortality during colonial times, is strongly associated

with current economic prosperity. The places where diseases were most

dangerous for Europeans are where we now find dysfunctional economic

systems and the most poverty, as well as the greatest corruption and

weakest rule of law. One important reason for this is the extractive

institutions that the European colonisers either established or chose to

keep, if it benefitted them.

Los galardonados de este año han añadido una nueva dimensión a las explicaciones anteriores sobre las diferencias actuales en la riqueza de los países de todo el mundo. Una de ellas está relacionada con la geografía y el clima. Desde que Montesquieu publicó su famoso libro El espíritu de las leyes (1748), existe la idea de que las sociedades de las zonas climáticas más templadas son más productivas económicamente que las de los trópicos. Y existe una correlación: los países más cercanos al ecuador son más pobres. Sin embargo, según los galardonados, esto no se debe únicamente al clima. Si eso fuera cierto, no podría haberse producido el enorme cambio de fortuna. Una explicación importante de por qué los países más cálidos son también más pobres es, en cambio, sus instituciones sociales.

Escaping the trap

Acemoglu, Johnson y Robinson han descubierto una clara cadena de causalidad. Las instituciones creadas para explotar a las masas son malas para el crecimiento a largo plazo, mientras que las que establecen libertades económicas fundamentales y el Estado de Derecho son buenas para él. Las instituciones políticas y económicas también tienden a ser muy longevas. Aunque los sistemas económicos extractivos proporcionen ganancias a corto plazo a una élite gobernante, la introducción de instituciones más integradoras, menos extractivas y el Estado de derecho crearía beneficios a largo plazo para todos. Entonces, ¿por qué la élite no sustituye simplemente el sistema económico existente?

The laureates’ explanation focuses on conflicts over political power

and the problem of credibility between the ruling elite and the

population. As long as the political system benefits the elites, the

population cannot trust that promises of a reformed economic system will

be kept. A new political system, which allows the population to replace

leaders who do not keep their promises in free elections, would allow

the economic system to be reformed. However, the ruling elites do not

believe the population will compensate them for the loss of economic

benefits once the new system is in place. This is known as the

commitment problem; it is difficult to overcome and means that societies

are trapped with extractive institutions, mass poverty and a rich

elite.

Sin embargo, los galardonados también han demostrado que la incapacidad de hacer promesas creíbles también puede explicar por qué a veces se producen transiciones a la democracia. Aunque la población de una nación no democrática carezca de poder político formal, dispone de un arma temida por la élite gobernante: son muchos. Las masas pueden movilizarse y convertirse en una amenaza revolucionaria. Aunque esta amenaza puede incluir la violencia, lo cierto es que la amenaza revolucionaria puede ser mayor si esta movilización es pacífica, porque permite que el mayor número de personas se una a las protestas.

Las élites se enfrentan a un dilema cuando esta amenaza es más aguda; preferirían permanecer en el poder y simplemente intentar aplacar a las masas prometiendo reformas económicas. Pero tal promesa no es creíble porque las masas saben que la élite, si permanece en el poder, puede volver rápidamente al viejo sistema una vez que la situación se haya calmado. En este caso, la única opción para la élite puede ser entregar el poder e introducir la democracia.

La introducción de instituciones más inclusivas, menos extractivistas y el Estado de Derecho generarían beneficios a largo plazo. Entonces, ¿por qué las élites no sustituyen simplemente el sistema económico existente?

El modelo de los galardonados para explicar las circunstancias en las que se forman y cambian las instituciones políticas tiene tres componentes.

-El primero es un conflicto sobre cómo se asignan los recursos y quién tiene el poder de decisión en una sociedad (la élite o las masas).

-El segundo es que las masas tienen a veces la oportunidad de ejercer el poder movilizando y amenazando a la élite dirigente; el poder en una sociedad es, por tanto, algo más que el poder de tomar decisiones.

-El tercero es el problema del compromiso, que significa que la única alternativa es que la élite ceda el poder de decisión a la población.

El modelo se ha utilizado para explicar el proceso de democratización en Europa Occidental a finales del siglo XIX y principios del XX. En Gran Bretaña, el sufragio se amplió en varias etapas, cada una de ellas precedida por huelgas generales y protestas generalizadas. La élite británica no pudo hacer frente de forma creíble a esta amenaza revolucionaria con promesas de reformas sociales, sino que se vio obligada, a menudo a regañadientes, a compartir el poder. La situación en Suecia fue similar, donde la decisión sobre el sufragio general en diciembre de 1918 se tomó después de amplios disturbios tras la revolución rusa. El modelo también se ha utilizado para explicar por qué algunos países alternan entre la democracia y la no democracia. También puede utilizarse para mostrar por qué es tan difícil para los países que no tienen instituciones inclusivas lograr un crecimiento igual al de los que sí las tienen, y por qué las élites gobernantes pueden beneficiarse a veces del bloqueo de nuevas tecnologías.

Daron Acemoglu, Simon Johnson y James Robinson han aportado investigaciones innovadoras sobre lo que afecta a la prosperidad económica de los países a largo plazo. Su investigación empírica demuestra la importancia fundamental del tipo de instituciones políticas y económicas que se introdujeron durante la colonización. Su investigación teórica ha contribuido a nuestra comprensión de por qué es tan difícil reformar las instituciones extractivas, al tiempo que señala algunas de las circunstancias en las que, no obstante, esto puede suceder. El trabajo de los galardonados ha tenido una influencia decisiva en la investigación continua tanto en economía como en ciencias políticas. Sus ideas sobre la influencia de las instituciones en la prosperidad demuestran que la labor de apoyo a la democracia y a las instituciones inclusivas es una importante vía para promover el desarrollo económico.

Further reading

Additional information on this year’s prizes, including a scientific

background in English, is available on the website of the Royal Swedish

Academy of Sciences, www.kva.se, and at www.nobelprize.org, where you

can watch video from the press conferences, the Nobel Lectures and more.

Information on exhibitions and activities related to the Nobel Prizes

and the Prize in Economic Sciences is available at

www.nobelprizemuseum.se.

The Royal Swedish Academy of Sciences has

decided to award the Sveriges Riksbank Prize in Economic Sciences in

Memory of Alfred Nobel 2024 to

DARON ACEMOGLU Born 1967 in Istanbul, Türkiye.

PhD 1992 from London School of Economics and Political Science, UK.

Professor at Massachusetts Institute of Technology, Cambridge, USA.

SIMON JOHNSON Born 1963 in Sheffield, UK. PhD

1989 from Massachusetts Institute of Technology, Cambridge, USA.

Professor at Massachusetts Institute of Technology, Cambridge, USA.

JAMES A. ROBINSON Born 1960. PhD 1993 from Yale University, New Haven, CT, USA. Professor at University of Chicago, IL, USA.

Science Editors: Tommy

Andersson, Peter Fredriksson, Jakob Svensson and Jan Teorell, members of

the Committee for the Prize in Economic Sciences in Memory of Alfred

Nobel. Illustrations: Johan Jarnestad Translator:Clare Barnes

Prize amount: 11 million Swedish kronor, to be shared equally between the laureates. Further information: www.kva.se and www.nobelprize.org Press contact: Eva Nevelius, Press Secretary, +46 70 878 67 63, eva.nevelius@kva.se Experts:

Tommy Andersson, +46 73 358 26 54, tommy.andersson@nek.lu.se, Peter

Fredriksson, +46 76 806 70 80, peter.fredriksson@nek.uu.se, Jakob

Svensson, +46 70 177 67 17, jakob.svensson@iies.su.se and Jan Teorell,

+46 70 868 18 91, jan.teorell@statsvet.su.se, members of the Committee

for the Prize in Economic Sciences in Memory of Alfred Nobel.

¿Cómo se forman las instituciones (políticas y económicas) y cómo afectan al comportamiento económico de un país?

Dos buenas preguntas que merecen un Premio Nobel en Economía ..

Lo que impulsó el cambio en Sudáfrica no fue la oposición blancos contra negros, ni entre burguesía y proletarios, sino entre quienes se beneficiaban del apartheid (propietarios agrícolas y mineros y trabajadores especializados blancos) y quienes se perjudicaban (propietarios industriales y de servicios, trabajadores no especializados y población negra).

They have helped us understand differences in prosperity between nations

Los galardonados de este año en ciencias económicas - Daron Acemoglu, Simon Johnson y James Robinson - han demostrado la importancia de las instituciones sociales para la prosperidad de un país. Las sociedades con un Estado de Derecho deficiente e instituciones que explotan a la población no generan crecimiento ni cambios a mejor. Las investigaciones de los galardonados nos ayudan a entender por qué.

Cuando los europeos colonizaron grandes zonas del planeta, las instituciones de esas sociedades cambiaron. El cambio fue a veces drástico, pero no se produjo de la misma manera en todas partes. En algunos lugares, el objetivo era explotar a la población indígena y extraer recursos en beneficio de los colonizadores. En otros, los colonizadores crearon sistemas políticos y económicos integradores para beneficio a largo plazo de los emigrantes europeos.

Los galardonados han demostrado que una de las explicaciones de las diferencias en la prosperidad de los países son las instituciones sociales que se introdujeron durante la colonización. A menudo se introdujeron instituciones inclusivas en países que eran pobres cuando fueron colonizados, lo que con el tiempo dio lugar a una población generalmente próspera. Esta es una razón importante de por qué las antiguas colonias que antes eran ricas ahora son pobres, y viceversa.

Algunos países quedan atrapados en una situación con instituciones extractivas y bajo crecimiento económico. La introducción de instituciones inclusivas crearía beneficios a largo plazo para todos, pero las instituciones extractivas proporcionan ganancias a corto plazo a las personas en el poder. Mientras el sistema político garantice que mantendrán el control, nadie confiará en sus promesas de futuras reformas económicas. Según los galardonados, por eso no se producen mejoras.

Sin embargo, esta incapacidad para hacer promesas creíbles de cambio positivo también puede explicar por qué a veces se produce la democratización. Cuando existe una amenaza de revolución, las personas en el poder se enfrentan a un dilema. Preferirían permanecer en el poder e intentar aplacar a las masas prometiendo reformas económicas, pero es poco probable que la población crea que no volverán al viejo sistema en cuanto se calme la situación. Al final, la única opción puede ser transferir el poder e instaurar la democracia.

"Reducir las enormes diferencias de renta entre países es uno de los mayores retos de nuestro tiempo. Los galardonados han demostrado la importancia de las instituciones sociales para lograrlo", afirma Jakob Svensson, Presidente del Comité del Premio de Ciencias Económicas.

“True, genuine, inclusive democracy matters, very clearly”

Simon Johnson, economic sciences laureate 2024, learnt of the award from

the congratulatory text messages piling-up on his phone. In this short

conversation, recorded just moments after he had heard the news, he

highlights the importance of participatory decision-making in making the

most of human potential.

https://www.nobelprize.org/

- Comprender la investigación ganadora del Nobel sobre instituciones y prosperidad

Claves de su investigación

Lección

clave: los países que crecen son aquellos en los que las instituciones

inclusivas salvaguardan los derechos políticos y económicos y limitan el

poder de las élites para expropiar los derechos de los ciudadanos.

Por su gran relevancia, extensión y variedad de temas, Nada es Gratis

dedicará varias entradas a comentar la obra de los recién galardonados

con el premio Nobel de economía Daron Acemoglu, Simon Johnson y James

Robinson, desde distintos ángulos y en sus diferentes vertientes. Aquí,

la primera de ellas.

El pasado lunes, Daron Acemoglu, Simon Johnson y James Robinson recibieron el premio Nobel de Economía por sus contribuciones al estudio de la formación de las instituciones y cómo estas afectan a la prosperidad de los países. El timing no podría haber sido más perfecto. Dos días antes había sido 12 de octubre.

Todo tiene que ver con todo.

Acemoglu se doctoró en la London School of Economics and Political

Science y actualmente es profesor en el departamento de economía en MIT.

Johnson es profesor en la Sloan School of Management, también en MI.

Por último, Robinson, quien alguna vez se definió como un “economista en

recuperación”, trabajó en los departamentos de ciencias políticas de

Berkeley y Harvard antes de unirse a la Harris School of Public Policy

de la Universidad de Chicago.

Los tres han publicado juntos y/o separados casi 300 artículos en

revistas de economía, ciencias políticas, finanzas e historia. Entienden

la economía como una ciencia social, rigurosa y multidisciplinar. La

obra de estos tres premiados es inabarcable, se mire por donde se la

mire. Permítanme hacer un recorrido parcial y breve por ella, inspirado

en el viaje de La Niña, La Pinta y La Santa María.

¿Qué tienen en común los galardonados con el “Día de la Hispanidad”?

Uno de los artículos más citados de estos autores, con más de 18,000

citas, se titula “The Colonial Origins of Comparative Development”. En él, investigan cómo las instituciones coloniales afectan la prosperidad de los países en la actualidad.

¿Pero cómo puede ser que instituciones establecidas hace 500 años

tengan algún efecto hoy en día? Simplificando, los autores argumentan

que hay dos tipos de instituciones: extractivas e inclusivas. Las

primeras benefician económicamente a una pequeña élite que también

ostenta el poder político (de jure y/o de facto). Dicha élite tiene incentivos a mantener el statu quo (es decir, las mismas instituciones) durante el mayor tiempo posible.

Por otra parte, las instituciones inclusivas reparten mejor el

pastel. Con un poder económico y político menos concentrado se facilitan

los acuerdos que benefician al conjunto de la sociedad, haciendo

aumentar su riqueza. Típicamente, se garantizan los derechos de

propiedad, lo que a su vez fomenta la inversión y el desarrollo.

En resumen, las instituciones de hoy dependen de quienes ostentaron poder (económico y político) ayer.

¿Y cuáles eran esas instituciones coloniales extractivas? Uno de los

ejemplos que mencionan los autores es el de las plantaciones de azúcar

en Brasil y el Caribe, cuyo objetivo era extraer la mayor cantidad de

recursos posible mediante el uso de mano de obra esclava. Otro ejemplo

es el de las minas del virreinato de lo que hoy es Perú. Melisa Dell,

una estudiante de Acemoglu, ha demostrado el efecto persistente de la

Mita, una institución utilizada por los colonos españoles que requería

trabajo forzoso en estas minas. Dell cuantificó el impacto negativo de la Mita en las instituciones y el desarrollo económico de las regiones afectadas y sus alrededores.

En otro artículo, titulado “Reversal of Fortune”,

Acemoglu, Johnson y Robinson fueron más allá y mostraron que la

revolución industrial acentuó las diferencias generadas entre países con

instituciones inclusivas o extractivas. Para poder aprovechar

innovaciones “científicas”, las sociedades debían proteger la inversión

en nuevas tecnologías.

Pero los ganadores del Nobel ya anticiparon nuestra siguiente

preguntar: Entonces, ¿las instituciones son inmutables? Su respuesta fue

“no”. En otro artículo multicitado,

Acemoglu y Robinson explicaron cómo una sociedad civil organizada puedo

lograr concesiones institucionales que aseguren una mejor distribución

de la riqueza. Cuando la élite se enfrenta a la posibilidad de perder el

poder, esta ofrece concesiones. Es decir, intenta otorgar beneficios a

quienes desafían su autoridad. En el siglo XIX, las élites de muchos

países occidentales introdujeron el voto universal como respuesta a la

amenaza de una revolución. De esta forma, el votante decisivo dejaba de

ser un miembro de estas élites y podía asegurar transferencias futuras a

su clase social. Este análisis sobre el conflicto y las concesiones

está desarrollado en mayor profundidad en su libro El pasillo estrecho, del que Gerard nos habló en su momento.

Hasta aquí he hablado de élites, clases sociales y poder económico y

político. Con esto no he querido sugerir que los recién premiados

aboguen por una revolución socialista (que yo sepa), pero sí que

entienden el devenir de las sociedades a través del conflicto de

intereses entre agentes con objetivos e incentivos distintos, que a su

vez se ven determinados en parte por las reglas y leyes del momento.

Como buenos agentes racionales, estos actores sociales también quieren

cambiar las reglas y leyes para favorecerse. Independientemente del

nombre que les demos a estos grupos, estudiar cómo las instituciones

resuelven el conflicto de interés entre ellos es clave para entender la

evolución histórica de las sociedades.

En el artículo que mencioné al principio, los tres premiados

mostraron que las instituciones coloniales determinan, en parte, las

instituciones actuales. En particular, utilizando la terminología

anterior, las instituciones coloniales inclusivas han contribuido a

aumentar la protección de la propiedad privada, disminuir el riesgo de

expropiación y fomentar el crecimiento. Yendo aún más al detalle del

artículo, la exogeneidad de las instituciones está dada por la

mortalidad de los colonos: en aquellas regiones donde los occidentales

tenían más probabilidad de sobrevivir, las instituciones fueron más bien

inclusivas. En cambio, en áreas con alta mortalidad (por ejemplo, por

malaria o fiebre amarilla) era más probable que las instituciones fueran

extractivas. Ademas del caso Latinoamericano, los autores también

exploraron las experiencias coloniales en África, como la del Rey

Leopoldo de Bélgica en el Congo.

En el segundo párrafo de ese mismo artículo, los autores escriben

“…que las instituciones son importantes no es una novedad”. En otras

palabras: Acemoglu, Johnson y Robinson no han ganado el Nobel por decir

que las instituciones son importantes. Lo han ganado por explicar, de

forma sistemática, cómo y por qué las instituciones son importantes,

cómo resuelven los conflictos, cómo determinan ganadores y perdedores. Y

cómo eso afecta el devenir de esas mismas instituciones, del

crecimiento económico y la desigualdad social. En cierto modo, han

complementado el trabajo de Ronald Coase,

quien recibió el Nobel por esclarecer el rol de los costes de

transacción y los derechos de propiedad dentro de las instituciones y la

economía. O el de Douglass North,

quien compartió el galardón con Fogel por haber contribuido a explicar

el cambio institucional desde un punto de vista histórico.

Acemoglu, Johnson y Robinson han escrito varios artículos sobre la

experiencia colonial, pero sobre éste, que nos provee de “una estimación

confiable de cuán importante son las instituciones”, Manuel Arellano ha escrito que se trata de “la regresión con variables instrumentales más importante de la historia”.

Todavía se habla de Cristóbal Colón y el nuevo mundo. De cómo ha

expandido la frontera de lo conocido, borrando los límites del viejo

mundo. A través de su obra, además de expandir el área de la economía

política, los recién premiados nos invitan a reflexionar sobre el avance

de la ciencia y la compartimentalización de la investigación, borrando

los límites entre historia, ciencia política y economía

Hoy segunda entrada de nuestra serie sobre las contribuciones de

los galardonados al premio Nobel de Economía 2024. Tras la entrada de Agustín Casas (CUNEF) ayer,

repasando algunos de los artículos más destacados de los premiados, hoy

damos la bienvenida a nuestro colaborador habitual y anterior editor

del Blog, José Luis Ferreira (UC3M), que nos ilustra sobre las vías de transmisión del conocimiento científico de los galardonados al gran público.

Muchos economistas han estudiado la interacción entre las

instituciones y la economía. Lo que distingue a estos tres galardonados

es el uso del análisis económico para sus investigaciones, haciendo

hincapié en los incentivos individuales a la hora de formular hipótesis y

modelos, y la búsqueda de validación estadística. Esto es distinto a lo

que, por ejemplo, hacía J.K. Galbraith, representante de la escuela de

economía institucional, cuando proponía que las relaciones entre grandes

empresas y gobierno obedece a dinámicas propias ajenas al mercado.

Partir de la premisa «las relaciones de poder importan» no es

formular una teoría, sino abrir una línea de investigación que puede dar

lugar a teorías muy distintas. Lo relevante es el poder explicativo de

cada una de ellas. Así, se puede desarrollar una teoría en términos de

lucha de clases, de grupos de presión, de coaliciones de interés, de

clanes o de castas, por poner unos ejemplos. Cada una de ellas deberá

mostrar un mecanismo causal explicativo y su alcance, es decir, el

conjunto de sociedades cuya evolución económica explica. De esta manera

podremos evaluar los méritos de cada una. Por poner un ejemplo, Acemoglu

y Robinson proponen que lo que impulsó el final del régimen de

apartheid en Sudáfrica no fue la oposición entre blancos y negros, ni

entre burguesía y proletarios, sino entre quienes se beneficiaban del

régimen y quienes se veían perjudicados. Los propietarios agrícolas y

mineros se beneficiaban de una gran cantidad de mano de obra que no

podía dedicarse a otras labores. Los propietarios industriales y de

servicios, más necesitados de mano de obra especializada, no podían

contratar para esos trabajos a trabajadores negros. Los trabajadores

blancos especializados no tenían competencia, los no especializados

tenían demasiada. Obviamente, la población negra era la gran

perjudicada. El cambio de régimen fue debido a la coalición de todos los

perjudicados, la alianza arcoíris.

Por qué fracasan los países

En este libro se recogen investigaciones como la anterior para

sostener la tesis principal: las instituciones explican el progreso de

las sociedades y sus cambios requieren coaliciones ganadoras que los

promuevan. En estas luchas, los ganadores podrán imponer instituciones

extractivas o inclusivas. Si las mafias, el estado, el colonizador o los

funcionarios corruptos se apoderan de gran parte de los ingresos de

trabajadores y empresarios ajenos al poder, los incentivos para invertir

en mejoras económicas serán muy pequeños. Las élites extractivas

tampoco tendrán incentivos en mejorar. Por una parte, encuentran

lucrativa la situación actual. Por otra, un cambio a otro tipo de

instituciones más inclusivas no garantiza su continuidad como parte de

las élites dominantes. No es fácil convencer a un grupo de familias que

dominan la economía de un país de que seguirán teniendo garantizadas sus

rentas en una economía más abierta.

Hay otras teorías sobre por qué unas sociedades son más ricas que otras. Por ejemplo, Dared Diamond, en su libro, Armas, gérmenes y acero

(1997), sostiene que las diferencias geográficas, con su influencia en

el clima, la biodiversidad y las comunicaciones, son la causa. Frente a

ello, Acemoglu y Robinson presentan numerosos casos en los que esa no

puede ser la explicación. Estos incluyen las diferencias entre las dos

Coreas y las dos Alemanias, entre los mexicanos que quedaron a uno y

otro lado de la frontera entre México y EE. UU., entre las regiones

peruanas del altiplano con diferentes instituciones coloniales en el

pasado y entre países vecinos como Botsuana y Zimbabue, por nombrar unos

casos. Otras teorías, como la diferencia cultural o religiosa son

igualmente rebatidas con este tipo de ejemplos y con otros en los que se

muestran sociedades que, sin cambiar cultura ni religión —ni, claro

está, geografía—, pero sí cambiando las instituciones, progresan o se

estancan según las nuevas que adopten.

El pasillo estrecho

Aquí, los autores desarrollan su teoría sobre las dinámicas que

subyacen a los cambios institucionales en una sociedad. Una sociedad con

un estado demasiado fuerte —una monarquía del antiguo régimen o un país

de la antigua Europa comunista— carecerá de un contrapeso en la

sociedad que presione para la adopción de instituciones inclusivas. En

el caso opuesto, un estado demasiado débil —una sociedad feudal o una

tribal— no podrá oponerse a los grupos de poder en la sociedad (clanes,

mafias o grandes propietarios, entre otros) ni proporcionar a la

sociedad los bienes públicos necesarios para su desarrollo. El pasillo

estrecho se refiere al equilibrio que debe haber entre el poder del

estado y el de la sociedad civil. Un país en el que las instituciones

civiles como medios de comunicación, centros de enseñanza, agrupaciones

culturales, sindicatos, etc., están al servicio del gobierno y su causa,

no tendrá una sociedad civil que controle mínimamente al estado. De ser

cierta esta teoría, comités de defensa de la república, de la

revolución o grupos paramilitares serían contrarios a este necesario

equilibrio en el estado que defenderían.

Acemoglu y Robinson repasan numerosos ejemplos históricos para

validar su teoría: países en que ha habido una revolución y países

aparentemente semejantes en los que ha habido cambios más graduales, y

también países a uno y otro lado del pasillo. Reconocen, sin embargo,

que un caso moderno podría refutar su teoría: China. Según ellos, al

carecer de una sociedad civil fuerte e independiente del estado, China

terminará estancándose. Su periodo de expansión tiene su analogía en el

desarrollo de la industria soviética tras la guerra. En este caso, el

progreso duró mientras extendía y adaptaba las tecnologías existentes,

pero terminó al ser incapaz de adoptar las nuevas de una manera

eficiente. Está por ver cómo será el caso chino, aunque de momento

parece no seguir claramente las predicciones de la teoría. Podemos ver

que China lidera en los sectores de baterías, vehículos eléctricos,

drones comerciales, robots industriales y de construcción, y

telecomunicaciones. Está atrás en farmacéutica, biología,

semiconductores, inteligencia artificial e informática. ¿Es esto

suficiente para decantarse de un lado o de otro? En la pandemia, este

país ofreció un ejemplo interesante. Por una parte, fue capaz de

construir grandes hospitales en muy poco tiempo, pero, por otra, tuvo

problemas para desarrollar una vacuna eficaz contra el Covid-19, en

comparación con las conseguidas por otros países.

Cómo valorar estas aportaciones

Juzgar si un trabajo particular de estos autores está mejor o peor

sustentado por la evidencia es la discusión normal en ciencia. Por

ejemplo, si para medir una diferencia en la protección de los derechos

de propiedad entre países se usa un índice imperfecto, el resultado que

se obtenga deberá ser leído con cautela y, en cualquier caso, mejorado

en cuanto se tengan datos más precisos. La polémica más importante, sin

embargo, se refiere al alcance de todos los trabajos acumulados para

sostener la tesis principal de la influencia de las instituciones en el

desarrollo, y en contraposición a otras influencias. Igual que estos

autores descartan la geografía como explicación, otros autores

encuentran casos de países con instituciones semejantes con desarrollo

desigual, o países en los que la geografía ha precedido y condicionado

las instituciones.

Llegados a este punto, echo en falta una discusión más ordenada. Las

distintas teorías que compiten para explicar las diferencias de

desarrollo entre las sociedades no tienen por qué ser excluyentes. Un

análisis empírico ideal nos diría, por ejemplo, qué parte de la riqueza

se explica por cada una de las distintas causas. El que no tengamos

datos para hacer este análisis no implica que debamos optar por una u

otra. Si acaso, iremos acumulando casos que lleven a concluir que una de

ellas es más importante en algunas circunstancias. Eso ya será mucho.

Permítanme concluir esta reseña con unas reflexiones acerca de cómo

leer este tipo de libros que parecen explicarlo todo. Algo que debe

evitarse hacer en todo momento es llegar a decir cosas del tipo: estoy

de acuerdo con el libro X, pero no con el Y. O bien, del libro Z estoy

de acuerdo con la aplicación de la tesis al caso A, pero no al B. Y debe

evitarse porque uno no es la vara de medir la verosimilitud de una

hipótesis. Las explicaciones que se dan en cada libro serán buenas en la

medida que los datos disponibles casen mejor con esas teorías que con

otras y, para eso, solo el contraste científico tendrá algo que decir.

Yo puedo leer el libro X y dejarme impresionar por su discurso, además

de encontrar lógicos y adecuados sus argumentos, pero mi opinión no

aportará un ápice de prueba a la evidencia científica. Por la misma

razón, el que yo concuerde en un primer momento con el libro tampoco

debería ser motivo para que yo mismo lo encuentre veraz, sino para

alertarme sobre posibles sesgos de confirmación. A no ser que yo sea un

experto en la materia, no es en la valoración de la teoría en donde debo

usar mi conocimiento, sino en la manera en que se ha desarrollado esta.

¿Son los datos presentados todos los relevantes? ¿Hay sesgos? ¿Qué

teorías alternativas se han descartado? Las explicaciones que yo veo

lógicas, ¿lo son en verdad? Para contestar a estas preguntas uno debe

saber qué filtros han pasado esas teorías. Después de leer a Acemoglu y

Robinson tendré que estar atento a confirmar si todos los episodios

relevantes en la historia económica de las naciones están recogidos en

el libro o si acaso se han dejado de lado algunos que no encajan en su

teoría.

1. Élites extractivas vs instituciones inclusivas.

2. Poder estatal vs poder social.

3. Poder vs tecnología

1.Élites extractivas vs instituciones inclusivas. Esta es la clave que relaciona instituciones y progreso. Las élites extractivas controlan la propiedad y las instituciones. Su interés principal es mantenerse como élites. Es un sistema ineficiente que impide el desarrollo

Podría pensarse que se les podría sobornar:

«Ahora ganáis 100, os garantizamos que seguiréis ganando esos 100 a cambio de que permitáis unas instituciones inclusivas».

Sin embargo, este contrato es difícil.

Una vez que existan nuevas élites, las viejas no tendrán garantizadas su supervivencia.

No es imposible. Los trabajos de Acemoglu y Robinson muestran cómo ha sucedido históricamente.

2. El estrecho corredor. Según esta tesis, estado y sociedad tienen que tener un equilibrio de poder y este tiene que responder a los intereses legítimos de cada parte

Un estado demasiado fuerte no es legítimo y terminará por acallar y atenazar a la sociedad y por caer en la corrupción. Un estado demasiado débil no podrá oponerse a los grupos de poder de la sociedad (clanes, mafias,…) ni proporcionar bienes públicos adecuadamente

El poder de la sociedad debe ser un contrapeso al del estado. Un estado sostenido por organizaciones que controlan la sociedad está en el comienzo de algunos totalitarismos del siglo XX (y alguno del XXI).

En España, hay partidos que quieren esto (procés, asalto al cielo…).

3. La tecnología no es suficiente. La tesis viene a decir que la tecnología puede beneficiar solo a una élite y ampliar las desigualdades sociales.

(su pesimismo sobre el impacto de las nuevas tecnologías y, más concretamente, la inteligencia artificial, no lo veo bien sustentado)

Todos los análisis se hacen teniendo en cuenta los incentivos de cada parte, grupo e individuo, sin caer en funcionalismos ingenuos y teniendo en cuenta el análisis económico.

Con métodos rigurosos y análisis histórico para incorporar la política a la comprensión de la economía (y viceversa).

Institutions as the Fundamental Cause of Long-Run Growth

D. Acemoglu, Simon Johnson, James A. Robinson

El documento analiza la importancia de las instituciones económicas como causa fundamental de las diferencias de crecimiento económico y prosperidad entre países. Sostiene que las diferencias en las instituciones económicas, más que la geografía o la cultura, son el principal motor de las disparidades de renta entre las naciones.

Las pruebas empíricas de los experimentos coreano y colonial sugieren claramente que las diferencias en las instituciones económicas, más que la geografía o la cultura, son el principal determinante de los resultados económicos a largo plazo.

El marco teórico subraya cómo los problemas de compromiso, la amenaza de los perdedores políticos y la inseparabilidad de la eficiencia y la distribución conducen a la aparición de instituciones económicas ineficientes que benefician a quienes detentan el poder."

The Colonial Origins of Comparative Development: An Empirical Investigation

D. Acemoglu, Simon Johnson, James A. Robinson

"El estudio pretende comprender las causas fundamentales de las grandes diferencias de renta per cápita entre países. Se centra en el papel de las instituciones y los derechos de propiedad como posibles determinantes del desarrollo económico.

Los investigadores encuentran una fuerte relación entre las tasas de mortalidad de los colonos y las instituciones actuales. Los lugares donde los colonos se enfrentaban a tasas de mortalidad más elevadas desarrollaron peores instituciones que protegían menos los derechos de propiedad. Utilizando la mortalidad de los colonos como instrumento, estiman un gran efecto de las instituciones en la renta per cápita. Su especificación más parsimoniosa sugiere que las diferencias en las instituciones pueden explicar alrededor de tres cuartas partes de las diferencias de renta entre países."

¿Cuál es la contribución de los nuevos premiados a la economía?

. ¿Por qué la calidad de las instituciones es fundamental para el desarrollo económico?

¿Qué posición ocupa España a nivel internacional?

¿Y qué importancia pueden tener en los bancos centrales y, en concreto, en el Banco de España estas aportaciones?

Hay países ricos y países pobres. Algunos de estos últimos consiguen progresar y desarrollarse desde posiciones retrasadas, como España o los países asiáticos en las últimas décadas. ¿Cuáles son las causas últimas de estas diferencias en la riqueza de los países? ¿Por qué fracasan los países?

La respuesta de los economistas galardonados es la calidad de las instituciones, que determinan la relación entre los que ostentan el poder (las élites gobernantes) y el resto de la sociedad. Cuanto mejores son, mayor es la prosperidad y mayores son las posibilidades de desarrollo económico.

Acemoglu, Johnson y Robinson distinguen entre dos tipos de instituciones:

Las instituciones inclusivas, que se fundamentan en el respeto de los derechos de propiedad y al Estado de Derecho y que suelen estar asociadas a sociedades democráticas. En estas instituciones las élites permiten a la ciudadanía desenvolverse, de forma que alcance sus objetivos económicos y sociales. De este modo, este tipo de institución incentiva los comportamientos que facilitan el buen funcionamiento de la economía, la creación de riqueza y el desarrollo de la sociedad civil. Y una sociedad civil fuerte demanda mejores instituciones, con lo que se genera un círculo virtuoso de crecimiento económico y progreso social (esquema 1).

Las instituciones extractivas, donde se conculcan derechos básicos y no hay seguridad jurídica. Aunque suelen ser más comunes en autocracias, también pueden estar presentes en democracias. En este caso, las élites persiguen extraer los recursos del resto de la sociedad para su propio beneficio. Este contexto limita el incentivo de la sociedad a generar riqueza, emprender e innovar y menoscaba el desarrollo social.

FUENTE: Banco de España.

Las instituciones inclusivas facilitan la creación de riqueza y el desarrollo de la sociedad civil, conformando un círculo virtuoso de crecimiento económico y social

Un punto importante que se deriva de su teoría es que la brecha de desigualdad entre las naciones no es fácil de cerrar. La fortaleza institucional puede activar un círculo virtuoso que favorece no solo el crecimiento económico, sino la mejora continua de las instituciones. Pero la debilidad institucional obstaculiza no solo el desarrollo, sino también el propio crecimiento institucional, lo que muchas veces impide cerrar la brecha.

Otro corolario es que las reformas, para que sean efectivas, requieren del contexto adecuado. Este punto lo probaron en un artículo sobre la independencia de los bancos centrales, precisamente. En las últimas décadas la mayoría de los bancos centrales se han convertido en independientes de los gobiernos. Y esta independencia se considera una de las razones para la reducción de la inflación en muchos países. Lo que demostraron los tres laureados es que en los países con instituciones extractivas los resultados en términos de control de la inflación fueron peores. La razón que dan es que las demandas de las élites seguían requiriendo un cierto nivel de distorsiones en los precios que acababan generando inflación.

¿Cómo romper el círculo vicioso entre instituciones y prosperidad? A través de los cambios en el equilibrio social. Un problema de las élites extractivas es la falta de confianza y credibilidad por parte del resto de la sociedad. Para mantener el poder están tentados a prometer cambios para mejorar el bienestar de la población, que raramente cumplen. Esta situación genera descontento, que puede acallarse con más opresión o, también, con la constatación por parte de la élite de la necesidad de reformas y de ceder parte del poder político a la ciudadanía. Estos cambios pueden darse de modo gradual y pacífico, como en las transiciones democráticas, o de repente y de modo convulso, como en las revoluciones.

Acemoglu y Johnson, en su reciente libro Poder y progreso, también han analizado el papel de la tecnología y la innovación en el crecimiento económico y, también en la configuración del poder. Por un lado, reconocen el efecto positivo del progreso tecnológico (democratizador) sobre las instituciones a lo largo de la historia. Por otro lado, alertan de que la revolución tecnológica actual, liderada por la internet y la inteligencia artificial, y concentrada en grandes corporaciones, puede tener un impacto negativo sobre el empleo y la propia calidad de la democracia.

¿Cómo ha evolucionado la calidad de las instituciones en España?

Desde hace 25 años, el Banco Mundial elabora unos Indicadores Globales de Gobernanza en los que valora cuatro grandes áreas de calidad institucional: el control de la corrupción, la efectividad del gobierno, la calidad regulatoria y el Estado de derecho. El análisis tiene un ámbito global y permite las comparaciones internacionales. Y el Banco de España está prestando cada vez más atención a estas cuestiones, a través de la investigación de sus economistas.

¿Cómo queda España en estas clasificaciones? El gráfico 1 muestra un retroceso. En la parte superior del gráfico se observa una caída en cada una de las cuatro áreas desde mediados de los años noventa. Y en la parte inferior se observa que, aunque la mayoría de los países ha registrado una pérdida de calidad institucional en los últimos años, la de España ha sido mayo. Esto supone una caída en la clasificación global y situarse por debajo de la media europea.

Gráfico 1 LA CALIDAD DE LAS INSTITUCIONES EN ESPAÑA SE HA REDUCIDO

FUENTE: Banco de España, Indicadores Globales de Gobernanza (Banco Mundial), BCENOTAS: Cada uno de los índices de calidad institucional, elaborados por el Banco Mundial, agrega varias dimensiones en una escala de -250 (baja calidad) a 250 (alta calidad). Una puntuación de 250 reflejaría que un países es el mejor una subcategoría específica o en las cuatro subcategorías mostradas.

La calidad institucional ha sufrido un retroceso en los últimos años a nivel global, pero en España ha sido mayorLa importancia de la calidad institucional ha ganado enteros en las últimas décadas, gracias a las contribuciones de los nuevos laureados. No obstante, algunas conclusiones son poco consistentes con lo que estamos observando últimamente. Por ejemplo, ¿cómo conciliar esta teoría y el fuerte desarrollo económico experimentado por distintas economías con regímenes no democráticos, como China? ¿O el retroceso institucional reciente en las democracias desarrolladas, contraviniendo la idea del círculo virtuoso? Todo ello no debilita la tesis principal de los Premio Nobel: que unas instituciones fuertes potencian el crecimiento. Es un recordatorio oportuno en estos tiempos inciertos y todas las instituciones públicas debemos trabajar para mejorar nuestra calidad

Estudios sobre cómo la calidad de las instituciones (entre ellas, los bancos centrales) influye en la prosperidad económica relativa de los países.

"Los países se convierten en Estados fracasados por el legado de las instituciones extractivas, (que) contribuyen directamente al fracaso del Estado al descuidar la inversión en los servicios públicos más básicos"

"¿Por qué el camino del cambio institucional difiere de una sociedad a otra? La historia es clave, ya que son los procesos históricos los que, a través de la deriva institucional, crean diferencias que pueden ser cruciales en coyunturas críticas"

"¿Qué se puede hacer para activar el desarrollo de instituciones inclusivas?". Proponen:

a) Cierto grado de orden centralizado

b) Instituciones políticas pluralistas

c) Control del poder

d) Papel determinante medios de comunicación (el autoritarismo lucha en su contra)

"La capacidad del Estado es su habilidad para conseguir sus objetivos, (y) depende en parte de cómo se organizan sus instituciones, pero de manera aún más decisiva depende de su burocracia, (que) tenga los medios y la motivación para (ejecutar) su misión"

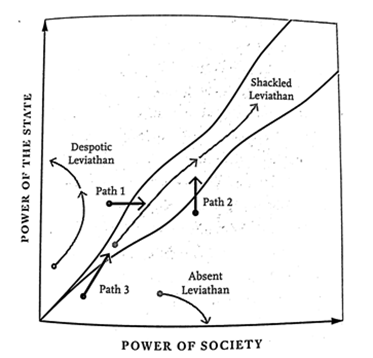

Leviatán "encadenado" (control del poder):

"Sus (políticos y) burócratas están sujetos a examen y supervisión. Es poderoso, pero coexiste con una sociedad a la que escucha y está atenta y dispuesta a implicarse en la política y a cuestionar el poder"

Leviatán "despótico":

"El Leviatán encadenado puede convertirse con rapidez en uno despótico. Necesitamos la competencia de la sociedad para mantener el Leviatán bajo control, y cuando más poderoso sea el Leviatán, más poderosa y vigilante debe hacerse la sociedad".

El Leviatán de "papel":

"El Leviatán de papel tiene algunas de las peores características de los leviatanes ausente y despótico. El Leviatán de papel con frecuencia no quiere controlar el saqueo, sino (que se manifiesta en) una economía plagada de corrupción"

Este capitulo 11, el de los leviatanes de papel, describe adecuadamente nuestra política y les expone a la lógica de restricciones al poder para tener sociedades incluyentes

La pregunta que se hacen estos autores conviene plantearla también en un contexto institucional tan degradado como el nuestro:

"¿A quién le gustan los controles y los contrapesos?"

Es obvio que nuestra clase política no los acepta, e incluso los desprecia con sus actuaciones

Roosevelt afirmó en 1944:

"La verdadera libertad no puede existir sin seguridad e independencia económica. Los hombres necesitados no son hombres libres. La gente que tiene hambre y está desempleada son el material con el que se hacen las dictaduras"

"Vivir con el Leviatán encadenado es una obra en marcha. (Hay que) crear y recrear el equilibrio entre el Estado y la sociedad, entre quienes tienen poder y quienes no. El poder de la sociedad tiene que ver con la organización y movilización social"

No es nuestro caso.

" ...las relaciones de poder importan» no es una teoría, es una línea de investigación que puede dar lugar a teorías muy distintas

Se puede desarrollar una teoría en términos de lucha de clases, de grupos de presión o de coaliciones de interés, entre otras. El poder explicativo de cada una será distinto y deberán evaluarse por ello " Jose Luis Ferreira

Las instituciones son cruciales, pero si la sociedad no tiene formas efectivas de controlar al gobierno, esas instituciones pueden volverse inútiles. Modelos de 4-5 hélices pueden ser mas efectivos. Las instituciones supranacionales deben ser reformadas cuando no cumplen sus objetivos

Resumen de R.Cobby:

El Nobel reconoce la importancia del análisis histórico y el papel de las instituciones en el desarrollo. Esto es clave, porque subraya que no solo las dinámicas económicas, sino las estructuras políticas, sociales y jurídicas, moldean el crecimiento de un país

El foco en instituciones nos permite entender el desarrollo como un proceso más complejo y multidimensional, algo que a menudo se pasa por alto en otros enfoques más cuantitativos o mecanicistas. Esto incluiría colonialismo e imperialismo, y su división desigual del trabajo

El trabajo de Acemoglu y cía. sitúa las clases sociales y los conflictos entre ellas en la evolución política y económica. Reconocen relaciones de poder no mercantiles, fuera de oferta y demanda

"Los conflictos entre élites, clases trabajadoras y otras fuerzas sociales han sido fundamentales para entender las transiciones históricas en las instituciones políticas y económicas, desde la Revolución Francesa hasta las luchas por los derechos laborales y de las mujeres

La crítica: Sin embargo, su visión del desarrollo en Occidente puede resultar simplista. Argumentan que el crecimiento en Europa y EE.UU. fue el resultado del respeto a los derechos de propiedad y mercados abiertos, pero esto no siempre fue siempre así.

Ejemplos como los enclosures en Inglaterra, los monopolios privados en varios sectores o la política industrial muestran que el desarrollo fue mixto, excluyendo a grandes sectores de la población o imponiendo medidas que no respetaban de forma universal los derechos de propiedad

Acemoglu, Robinson y Johnson han hecho contribuciones valiosas al resaltar la importancia de instituciones y conflictos sociales en el desarrollo.

Pero su visión de cómo ocurre en la práctica, tanto en Occidente como en el resto del mundo, no coincide con el registro histórico

Su marco no explica bien el auge de Asia Oriental, China y su rápida innovación tecnológica. Aquí es donde otros economistas y especialistas en desarrollo como Alice Amsden, Mushtaq Khan, Ha-Joon Chang,@yuenyuenango Erik Reinert ofrecen una visión del mundo real." Roy Cobby

"Estos autores destacan que el éxito de China no se ajusta al guion de instituciones "inclusivas" en el sentido occidental, sino a un enfoque más complejo de desarrollo, que incluye intervenciones estatales estratégicas y una gestión de las élites muy distinta al puro mercado"

https://x.com/RoyCobby/status/1846107268862935061

Es capitalismo de estado, un modelo dual, interveniendo con ingenieria económica donde interese para ser competitivos, y con su sobreproducción poder inundar con sus productos a Occidente, desindustrializandolo por no tener Europa una política industrial

¿Huy una limitada capacidad del estado de organizar la economía?. Es una crítica desatinada en los trabajos sobre instituciones extractivas vs inclusivas o en la tesis del «estrecho corredor» Si el estado permite el libre comercio, esto es una institución que no necesita de un estado con capacidades extraordinarias de organizar la vida económica de la sociedad

El ejemplo es China, con sus planes quinquenales organizando su economica, es un capitalismo de estado,

han pasado en dos decadas del modelo parasitario al modelo tecnologico, incentivando la

sobreproducción para inundar Occidente sin posibilidad de competir, con

una OMC sin actuar de forma precisa

Es más atinada la crítica cuando se centra en las conclusiones de lo que puede hacer el estado con respecto al desarrollo, extensión y uso de las nuevas tecnologías.

El Premio Nobel de Economía 2024, otorgado a Daron Acemoglu, Simon Johnson y James A. Robinson, llega en un momento crítico para la evolución de la sociedad y economía mundial. En un momento de fuerte desapego social

“En todos los debates de desarrollo económico y crecimiento hay algo del ‘huevo y la gallina’. Por ejemplo, si vos tenés tecnología de avanzada, entonces crecés más, o si es porque sos rico que podés invertir más en tecnología. Ellos lo que propusieron fue un zoom out, y buscan el último factor exógeno real, para separarse de las cuestiones endógenas de la economía, y llegan a la generación de instituciones fundacionales de un país”, dice Judzik, sobre un aporte en el que los autores trabajaron en diferentes papers académicos, analizando fundamentalmente la historia moderna de algunos países y el rol de la colonización.

“Eso no quita que haya factores macroeconómicos que empujan ese sendero de crecimiento, para bien o para mal, pero, en promedio y de largo plazo, sostienen que ese desarrollo lo explican las instituciones”, agrega el docente de UTDT.

Para Andrés López, titular de la cátedra de Desarrollo Económico en la facultad de Ciencias Económicas de la UBA y director del IIEP, el aporte de los ganadores del Nobel 2024 fue haberrenovado el interés por el estudio del rol de las instituciones

“Lo que plantean tiene tres claves. Primero, es cierto que los economistas creen que el crecimiento viene del capital humano, el progreso tecnológico y la inversión en capital, pero todo eso depende de factores últimos que hacen que haya más o menos progreso e inversión, y eso son las instituciones, las reglas de juego. Segundo, que esas instituciones se explican por procesos históricos, y que el origen pueden ser los procesos de colonización. Y tercero, que cuando las instituciones son disfuncionales para el crecimiento, pueden ser difíciles de cambiar, y por eso la persistencia de los países pobres”, resume López.

“Acemoglu está preocupadísimo por la desigualdad y la marginación social que va a traer la aplicación masiva de la IA en los procesos productivos, y su impacto distributivo”, dice Judzik, quien retoma algunas de las ideas sobre el tema en Automatizados, el libro publicado este año junto a Eduardo Levi Yeyati.

Los receptores del premio Nobel en economía de 2024, D. Acemoglu, S.

Johnson y J. Robinson, han proporcionado una interpretación de las

diferencias que se observan en el grado de progreso económico entre

distintas regiones y países, así como de su persistencia en el tiempo,

apelando a la calidad de su estructura institucional como un factor

determinante. A su juicio, otros factores que se han aducido como

explicativos del distinto grado de desarrollo, como la localización

geográfica, o los avances culturales, están relacionados con la

estructura institucional de los países, pero no pueden explicar las

diferencias observadas en el progreso de los países sobre periodos

dilatados de tiempo.

Su investigación sobre este tema, realizada lo largo de décadas, se

basó inicialmente en el examen de las experiencias de colonización de

amplias regiones del mundo por parte de países europeos. Observaron que,

en regiones altamente pobladas, en las cuales la resistencia a la

colonización podía ser mas fuerte, el propósito de los colonizadores fue

explotar la fuerza de trabajo aportada por la población indígena y

extraer sus recursos naturales. La elevada densidad poblacional también

favorecía la expansión de enfermedades, generando una mortalidad

elevada. No pudiendo consolidar su permanencia masiva debido a la alta

mortalidad, los colonizadores se asociaron con una élite local para

llevar a cabo su experiencia colonizadora, basada en instituciones

extractivas, y generando un beneficio para los países colonizadores

durante un período relativamente corto.

En otras zonas, generalmente menos densamente pobladas, hubo menor

mortalidad y mayor número de colonizadores, quienes pudieron construir

sistemas económicos y políticos inclusivos, en beneficio de la población

local. En estos casos, los países colonizadores obtuvieron un beneficio

más duradero.

La diferencia de estructura institucional tuvo un efecto

trascendental a largo plazo: las regiones más pobladas, inicialmente más

ricas, prosperaron poco y son hoy regiones menos ricas; cuentan

actualmente con instituciones económicas y políticas de menor calidad, y

mayores niveles de corrupción. Por el contrario, las que estaban

inicialmente poco pobladas y contaban con pocos recursos, son hoy

algunas de las áreas más prósperas, y cuentan generalmente con

instituciones económicas y políticas de mayor calidad, y menores niveles

de corrupción política y legal.